by Kate Pearce

Each quarter, a team of wireless analysts at Compass Intelligence comb through financial documents to analyze, define and make sense of the wireless industry by collecting and collocating metrics and facts. To do this, we peruse the financials of the four major carriers and many of the regional providers. This includes 10-Q reports, carrier earnings presentations, banking reports and earnings transcripts. We seek to compare metrics and identify changes/trends in the industry to help formulate a better story for our clients. Here is a snapshot of some of the things what we saw in 3Q 2014.

Each quarter, a team of wireless analysts at Compass Intelligence comb through financial documents to analyze, define and make sense of the wireless industry by collecting and collocating metrics and facts. To do this, we peruse the financials of the four major carriers and many of the regional providers. This includes 10-Q reports, carrier earnings presentations, banking reports and earnings transcripts. We seek to compare metrics and identify changes/trends in the industry to help formulate a better story for our clients. Here is a snapshot of some of the things what we saw in 3Q 2014.

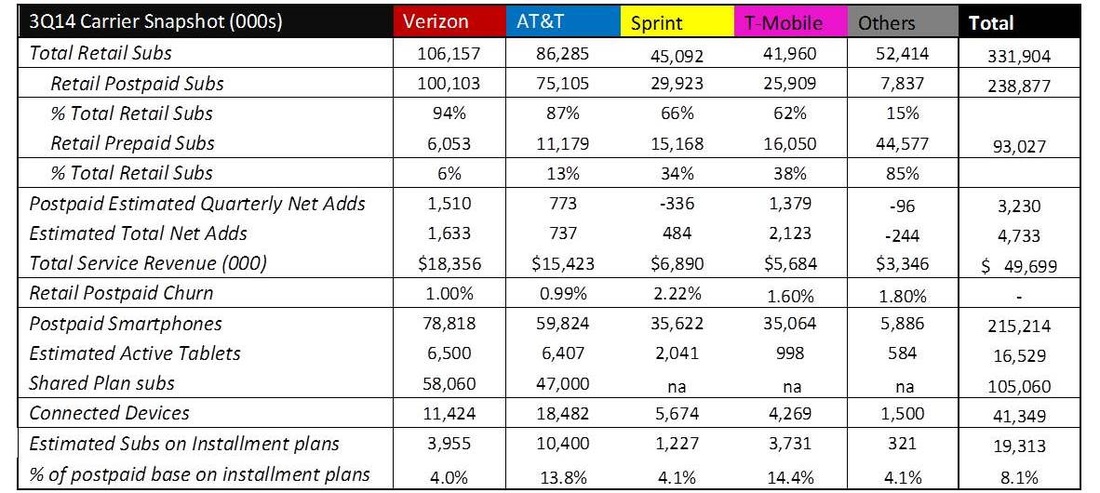

The table above is a compilation of key 3Q 2014 metrics around retail subscribers, churn, advanced device subscriber base, share/installment plans and more.

Some of the overall themes in the industry driving net additions and lower churn include:

Verizon

Overall, the industry added new subscribers (we estimate about 4.7M net additions) with many of these being tablets (we estimate over 2M were new tablet additions). Installment plans are gaining more traction. We estimate over 19M subscribers on installment or early upgrade plans. AT&T is leading this charge as the carrier seeks to move completely away from handset subsidies as a way to improve its bottom line. However, as the industry continues to mature, each of the wireless carriers will need to become increase focus on retaining customers with improved network coverage and customer care. Verizon has been doing this with network improvements and cutting costs internally. Overall, the mobile carriers will also need to offer additional services to create new revenue streams, such as in-home connectivity, wearables and in-car solutions.

For more information or to access our new report on 3Q 2014 Subscriber Tracking Report, please contact Kate Pearce at [email protected].

Some of the overall themes in the industry driving net additions and lower churn include:

- Aggressive pricing with new monthly plans

- Increased data buckets

- New flagship smartphone and tablet models entering the market

- Installment plans (moving away from the handset subsidy model)

- Tablet growth

Verizon

- Another strong quarter for Verizon where the company surpassed 100M retail postpaid subscribers for the first time.

- The company reported over 1.5M postpaid net adds, largest in the industry.

- Verizon says profitability is coming from lower churn (focused on customer retention), company efficiencies and growth is via strong tablet sales.

- Verizon also reported is had 6.5M active tablets.

- AT&T posted good overall net additions and the lowest postpaid churn in the industry.

- The company is more aggressive with Next than other carriers. AT&T said that it added another3.4M subscribers to its Next program, making the total over 10M.

- AT&T also said it had 47M subscribers on its share plans

- The carrier also reported over 18M connected devices (wearables, tracking, in-car) on its network.

- Sprint continued to struggle with adding customers. It reported over 330K postpaid net losses.

- The company is still adding customers in the wholesale and M2M channels, however.

- Sprint is starting to get more aggressive with pricing, so we may see an uptick in 4Q14.

- The carrier reported 2.22% retail postpaid churn, which was the highest among the four major carriers.

- T-Mobile reported another stellar quarter, adding 2.1M total additions which led the industry.

- The company is also continuing to lower churn and reported 1.6% postpaid churn.

- T-Mobile is reporting strong smartphone adds but is still lagging in tablet subscribers. We estimate the carrier has around 1M total activated tablets.

- "Other" consists of carriers like Tracfone, US Cellular, Cincinnati Bell Wireless and Alaska Digital.

- Many of these carriers are losing subscribers as the larger carriers pricing plans and coverage is very competitive.

- Major prepaid carriers like Tracfone continue to add subscribers.

Overall, the industry added new subscribers (we estimate about 4.7M net additions) with many of these being tablets (we estimate over 2M were new tablet additions). Installment plans are gaining more traction. We estimate over 19M subscribers on installment or early upgrade plans. AT&T is leading this charge as the carrier seeks to move completely away from handset subsidies as a way to improve its bottom line. However, as the industry continues to mature, each of the wireless carriers will need to become increase focus on retaining customers with improved network coverage and customer care. Verizon has been doing this with network improvements and cutting costs internally. Overall, the mobile carriers will also need to offer additional services to create new revenue streams, such as in-home connectivity, wearables and in-car solutions.

For more information or to access our new report on 3Q 2014 Subscriber Tracking Report, please contact Kate Pearce at [email protected].

RSS Feed

RSS Feed