By Kate Pearce

At Compass Intelligence, one of the areas we've focused on in the last few years is around detailed tracking of the mobile carriers key subscriber metrics. Listening to earnings calls, combing through quarterly/annual reports and keeping close account of speeches to Wall Street are a few of the ways we gather this imperative competitive intelligence.

One of the outputs of this constant monitoring is our carrier tracking deliverable aka the End of Year Carrier Results: A Comprehensive Guide to Key Carrier Metrics, 4Q2012-4Q2014 report. It really is a helpful quarterly historical view of the wireless industry that shows changes quarter over quarter in the sometimes fast-paced mobile environment. Foundational analysis like detailed carrier tracking can also provide insights and offer key indicators about movements that are slower in nature as well. This report, while tracking overall subscriber growth over time, also provides breakouts by carrier for overall connections, wholesale subscribers, postpaid, prepaid, device types and more. We also track “hot” metrics around early upgrade or installment plans offered by the carriers. Finally, the report shows overall tablet subscribers by carrier as well as smartphone and feature phone breakouts.

At Compass Intelligence, one of the areas we've focused on in the last few years is around detailed tracking of the mobile carriers key subscriber metrics. Listening to earnings calls, combing through quarterly/annual reports and keeping close account of speeches to Wall Street are a few of the ways we gather this imperative competitive intelligence.

One of the outputs of this constant monitoring is our carrier tracking deliverable aka the End of Year Carrier Results: A Comprehensive Guide to Key Carrier Metrics, 4Q2012-4Q2014 report. It really is a helpful quarterly historical view of the wireless industry that shows changes quarter over quarter in the sometimes fast-paced mobile environment. Foundational analysis like detailed carrier tracking can also provide insights and offer key indicators about movements that are slower in nature as well. This report, while tracking overall subscriber growth over time, also provides breakouts by carrier for overall connections, wholesale subscribers, postpaid, prepaid, device types and more. We also track “hot” metrics around early upgrade or installment plans offered by the carriers. Finally, the report shows overall tablet subscribers by carrier as well as smartphone and feature phone breakouts.

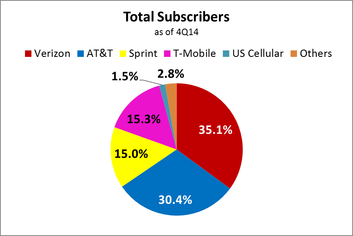

Source: Compass Intelligence, 2015

Key themes from the latest quarter are around new smartphone and tablet launches and pricing, installment plan growth, tablets and the focus on B2B, including data and international plans.

Here are some other takeaways from the report:

· Total subscribers were 331 million at the end of 2014. Verizon leads in share with 35.1% and AT&T is #2 at 30.4% share.

· The interesting race is with 3rd and 4th. Looks like T-Mobile (15.3%) surpassed Sprint (15.0%) in Total Subscriber share in 4Q14.

· Tablet activations continued on the upward growth trajectory. The industry ended 3Q14 with about 16.4 million active tablets and this quarter that number grew to over 19.8M.

As you can see from these stats, the mobile industry is shifting (this gets really interesting from a foundation standpoint). As we all know, 2014 was a year of hyper-competition. Pricing wars, installment plans, no more contracts, etc. were just a few of the areas of the business that really took off. And, 2015 should not disappoint either. Not only will it be interesting to see overall how the industry metrics change due to big changes like handset subsidy reduction and tablet focus, but also how will each of the carriers fair. One big question: Can T-Mobile maintain the growth trajectory it set in 2014? Will Sprint continue to rebound? Will Verizon stay impenetrable (relatively) and is AT&T going to take the B2B segment to another level? All in all, it should be another fun year and we plan to answer these questions and more…one metric at a time.

For more information on this report or any from our Mobile & Wireless subscription, please contact Kate Pearce at [email protected]

Here are some other takeaways from the report:

· Total subscribers were 331 million at the end of 2014. Verizon leads in share with 35.1% and AT&T is #2 at 30.4% share.

· The interesting race is with 3rd and 4th. Looks like T-Mobile (15.3%) surpassed Sprint (15.0%) in Total Subscriber share in 4Q14.

· Tablet activations continued on the upward growth trajectory. The industry ended 3Q14 with about 16.4 million active tablets and this quarter that number grew to over 19.8M.

As you can see from these stats, the mobile industry is shifting (this gets really interesting from a foundation standpoint). As we all know, 2014 was a year of hyper-competition. Pricing wars, installment plans, no more contracts, etc. were just a few of the areas of the business that really took off. And, 2015 should not disappoint either. Not only will it be interesting to see overall how the industry metrics change due to big changes like handset subsidy reduction and tablet focus, but also how will each of the carriers fair. One big question: Can T-Mobile maintain the growth trajectory it set in 2014? Will Sprint continue to rebound? Will Verizon stay impenetrable (relatively) and is AT&T going to take the B2B segment to another level? All in all, it should be another fun year and we plan to answer these questions and more…one metric at a time.

For more information on this report or any from our Mobile & Wireless subscription, please contact Kate Pearce at [email protected]

RSS Feed

RSS Feed